TRD Issue 89 - Briefing: Meta's AI Strategy, Walmart's Unique Position, and E-commerce's New Reality

Meta's Llama faces cloud adoption challenges as e-commerce software startups pivot business models. Meanwhile, TikTok's "super-app" ambitions threaten specialized platforms.

Hello Subscribers,

Meta's making an interesting AI play, trying to position Llama as the industry standard while negotiating cloud partnerships, but facing mixed results on AWS where Anthropic's Claude is winning more business.

Speaking of giants, Walmart's strong results shouldn't fool investors looking at broader retail—their grocery-heavy business model and high-margin side hustles make them a poor indicator for other retailers. Meanwhile, Circle K's parent company is attempting what analysts call a "pipe-dream" $38B acquisition of 7-Eleven's parent that would create a convenience store behemoth controlling nearly 20% of the US market.

On the e-commerce front, we're seeing a major shakeout among software startups that boomed during the pandemic. Companies like Attentive and Loop Returns are pivoting their business models as growth slows—expand offerings or become acquisition targets.

The most fascinating thing might be TikTok's "Everything War" in Southeast Asia, which expanded from e-commerce to local services (restaurants, hotels, etc.) in Indonesia and Thailand. Could be a legitimate super-app threat to specialized platforms like Grab and Agoda.

What are you seeing in your corner of the industry?

The Retail Direct

About 91APP

Founded in 2013, 91APP is the premier OMO (online-merge-offline) SaaS company, providing one-stop omnichannel retail solutions in Taiwan, Hong Kong, and Malaysia. It offers advanced Commerce Solutions and Marketing Solutions that enable retail brands to penetrate the D2C (Direct-to-Consumer) e-commerce market and drive operational benefits to their full potential. In 2021, 91APP became the first SaaS company to be listed in Taiwan and has been named one of Taiwan's "NEXT BIG" companies by Startup Island TAIWAN.

For more information about 91APP (TWO: 6741), visit 91app.com.

AI

Meta's AI Push Requires New Enterprise Sales Strategy

Why it matters: Meta's ambition to make Llama the industry standard for AI depends on a rapid pivot to enterprise sales — an area where the company has limited experience and current partnerships with cloud providers yield mixed results.

Meta's Llama 3 model faces several hurdles:

- Trails rivals like Anthropic's Claude on AWS

- Ranks behind OpenAI and Google in independent evaluations

- Relies on cloud partners for enterprise distribution

Despite not directly charging for its open-source LLMs, Zuckerberg revealed revenue-sharing deals with "major cloud companies" selling Llama, positioning it as a lower-cost alternative to proprietary models like OpenAI.

What's happening now:

- Meta is negotiating a potential $1B+ AWS expansion deal

- In talks with Snowflake to allow custom Llama training

- Goldman Sachs spending $1M+ on Llama via Azure

Meta's enterprise strategy draws comparisons to Linux's industry-standard approach, with Zuckerberg building "massive infrastructure," including orders for 350,000 Nvidia H100 chips to support the AI push.

Source: The Information

BigCommerce Bets on Google-Powered AI to Compete in E-Commerce

Why it matters: Struggling e-commerce platform BigCommerce is leveraging Google Cloud's AI to revitalize its business, delivering measurable results as it competes with industry giants like Shopify while fighting to reverse years of financial losses.

The Austin-based company unveiled several AI tools to help merchants boost sales:

- Real-time personalized product recommendations (20% increase in click-through rates)

- AI-generated custom quote proposal emails for B2B sales

- SEO-optimized product descriptions in brand voice

- Coming soon: semantic search and predictive analytics

Despite losing 90% of its market value since its 2020 IPO and multiple rounds of layoffs, BigCommerce reported 24Q2 revenue up 8% to $82M while narrowing losses to $11M (down from $19M year-over-year).

The bottom line: The company differentiates itself through platform openness, allowing merchants to choose from both native Google-powered AI features and third-party AI solutions based on specific business needs.

Source: Modern Retail

Retail

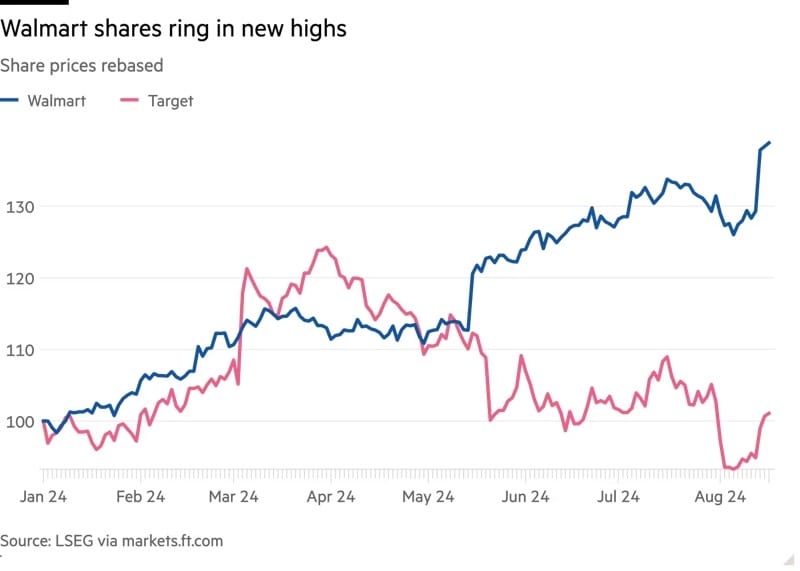

Walmart's Strength Masks Broader Retail Struggles

Why it matters: Walmart's impressive 24Q2 performance reflects its unique position in retail rather than industry-wide health, making it a potentially misleading bellwether for investors betting on other retailers.

Walmart's distinct advantages are driving its outperformance:

- Massive grocery business (60% of US revenue) benefits from inflation-conscious shoppers

- Higher-income consumers trading down for groceries

- Growing high-margin side businesses, including marketplace, digital ads, and membership programs.

The numbers tell the story:

- Walmart's like-for-like sales are up 4.2% vs Home Depot down 3.6%

- Food prices up 25% between 2019-2023, faster than most categories

- Walmart stock up 40% this year, trading at 29x forward earnings

The bottom line: Investors who pushed up shares of Target, Macy's, and Gap following Walmart's results may face disappointment as these retailers lack Walmart's scale, grocery focus, and diversified revenue streams.

Source: FT

Massive Circle K-7-Eleven Deal Faces Multiple Hurdles

Why it matters: The proposed acquisition of Seven & i Holdings (7-Eleven's parent) by Circle K owner Alimentation Couche-Tard would create a convenience store behemoth controlling nearly 20% of the U.S. market but faces significant regulatory and stakeholder opposition.

The deal would reshape the convenience store landscape:

- The combined company would control over 100,000 stores globally

- In the U.S., 7-Eleven holds a 14.5% market share while Circle K has a 4.6%

- The acquisition would give Circle K massive pricing power and data advantages

Experts are skeptical, despite Couche-Tard's aggressive expansion strategy (recently buying GetGo's 270 gas stations and 2,000+ European stores):

- Japanese analyst Michael Causton calls it a "pipe-dream bid"

- Influential Ito family (8.1% stake worth $3.1B) likely to oppose

- Japanese government concerns about foreign ownership of crisis-response infrastructure

- Potential U.S. regulatory scrutiny similar to Couche-Tard's failed $20B Carrefour bid

The bottom line: Seven & i has been under pressure from major shareholder ValueAct Capital to restructure and focus on growing its convenience store business. The company has formed a special committee to review the proposal.

Source: Modern Retail

Athletic Retailers Transform Stores into Experiential Destinations

Why it matters: Major athletic retailers invest heavily in immersive store concepts to combat online competition and increase in-store sales, with early adopters reporting higher traffic, conversion rates, and larger basket sizes.

Foot Locker's "Store of the Future" and Dick's "House of Sport" locations are leading this trend with interactive features that capitalize on consumers' preference for in-person shopping (58% prefer in-store for apparel and footwear).

Key innovations include:

- Foot Locker: foot-scanning stations, sneaker customization bars, digital jump-measurement screens

- Dick's: rock climbing walls, batting cages, larger formats

- Nike: "World of Flight" stores with customization areas and lounges

Both companies report promising results: Foot Locker's first redesigned store is now among its top North American locations, while Dick's reports customers driving further and spending more time in its experiential formats.

The bottom line: These investments align with broader retail strategy shifts to combat online discounting from Amazon and Temu while capitalizing on in-store purchasing behavior, which typically generates higher average baskets than e-commerce channels.

Source: Modern Retail

e-Commerce

Ikea Launches Secondhand Marketplace to Tap Growing Resale Market

Why it matters: Ikea's new "Preowned" marketplace positions the furniture giant to capture a slice of the rapidly growing secondhand furniture market, where Ikea products already make up 10% of transactions happening on third-party platforms.

The pilot program, currently testing in Madrid and Oslo, allows sellers to list used Ikea items with AI assistance that automatically populates product details and dimensions from Ikea's database.

Key features of the marketplace:

- Sellers can choose between cash payment or Ikea vouchers with a 15% bonus

- Listings are currently free, though a "symbolic" fee may be introduced later

- The secondhand furniture market is projected to grow by 6.4% in 2024

Ikea CEO Jesper Brodin calls the marketplace "a dream in the making," noting it represents the company's evolution in digital capabilities while potentially reconnecting with former customers through the resale process.

The bottom line: If successful beyond the test markets, Ikea Preowned could expand globally to compete directly with eBay, Gumtree, and similar platforms in 2025.

Source: Business Insider

E-commerce Software Startups Face Consolidation as Growth Slows

Why it matters: E-commerce software providers are struggling with slowing growth and market saturation after pandemic-era success, forcing them to pivot business models or become acquisition targets.

Companies feeling the pressure:

- Attentive (SMS marketing): Projected $600M ARR for 2023 but hit only $460M, struggling to reach IPO readiness

- Loop Returns: Revenue growth dropped from nearly 100% to 30%, laid off 20% of staff last week

The market is facing multiple challenges:

- Slowing e-commerce growth post-pandemic

- Merchant cost-cutting amid consumer spending pullback

- Feature overlap among crowded competitors

- Business model shifts (moving costs from merchants to customers)

Consolidation has already begun with Trove acquiring Recurate and Shopify, buying smaller startups like Peel Insights and Checkout Blocks. Experts predict companies with broader service offerings will survive, while specialists become acquisition targets for PE-controlled platforms like Bazaarvoice.

The bottom line: To survive, companies are expanding beyond core offerings - Attentive to adding AI products and email marketing, Loop shifting fees to shoppers - as they race to reach profitability before the funding runway expires.

Source: The Information

Asia

Walmart Exits JD.com as China's E-commerce Landscape Shifts

Why it matters: Walmart's complete divestment from JD.com reflects the declining strategic value of Chinese e-commerce partnerships amid market fragmentation, slowing growth, and new retail channels.

Walmart's stake liquidation (worth ~$3.6B) sent JD.com shares plunging 10% in Hong Kong trading, mirroring a similar drop when Tencent divested most of its JD.com holdings in 2021.

Key factors driving Walmart's exit:

- Diversified e-commerce landscape with livestream commerce taking market share

- Industry-wide growth slowdown and margin pressure from price wars

- Walmart's established physical presence (400+ stores) and multiple online channels

Chinese e-commerce stocks have lost significant value, with JD.com down 75% from its 2021 peak and trading at just 7x forward earnings versus Amazon's 35x, signaling continued investor skepticism about the sector's prospects.

Source: FT

India's ONDC Could Disrupt E-commerce Models Across Asia

Why it matters: India's Open Network for Digital Commerce (ONDC) aims to break the Amazon-Flipkart duopoly by creating an open e-commerce ecosystem where buyers can access multiple seller platforms through any app — potentially offering a model for Southeast Asian markets dominated by Shopee and Lazada.

Despite minimal market impact after two years, ONDC has:

- 535,000 sellers (85% small merchants)

- 65 seller apps, 12 logistics providers, 22 buyer apps.

- Major participants include Snapdeal, Meesho, Ola, and Tata Neu.

- Sparked interest from Singapore, Indonesia, and Malaysia

The network faces significant challenges:

- Limited logistics coverage in many regions

- Commission model still evolving (currently 10-12% less than major platforms)

- Consumer experience lags behind established players in pricing and delivery times

The bottom line: ONDC's potential as a "duopoly breaker" remains uncertain, with experts suggesting it follow UPI's path (which took years to reach 75% of digital transactions) and focus on establishing itself in India before expanding regionally.

Source: Tech in Asia

TikTok Expands from E-commerce to Local Services in Southeast Asia

Why it matters: After disrupting e-commerce in Southeast Asia with TikTok Shop, the platform tests local services in Indonesia and Thailand, potentially creating a super-app that could threaten specialized platforms like Grab and Agoda.

Building on Douyin's success in China (256% GMV growth in local services), TikTok is leveraging its massive regional user base (325 million monthly users) to connect consumers with restaurants, hotels, and physical businesses through its addictive video feed.

Key advantages of TikTok:

- More fragmented market with no clear leader across categories

- Strong video consumption habits in Southeast Asia

- Location-based video and live-streaming capabilities

- Higher margins on digital goods compared to e-commerce

Major challenges remain:

- Delivery logistics less developed than in China

- Requires building new partnerships beyond J&T Express

- Resource allocation between e-commerce and local services

Analysts predict this signals the start of an "Everything War" where platforms must expand across the value chain or risk displacement, with local services potentially contributing 15-20% of TikTok's revenue in the region.

Source: Tech in Asia

Comments ()